The best quarter since 2020 just closed — here's what decides the next one

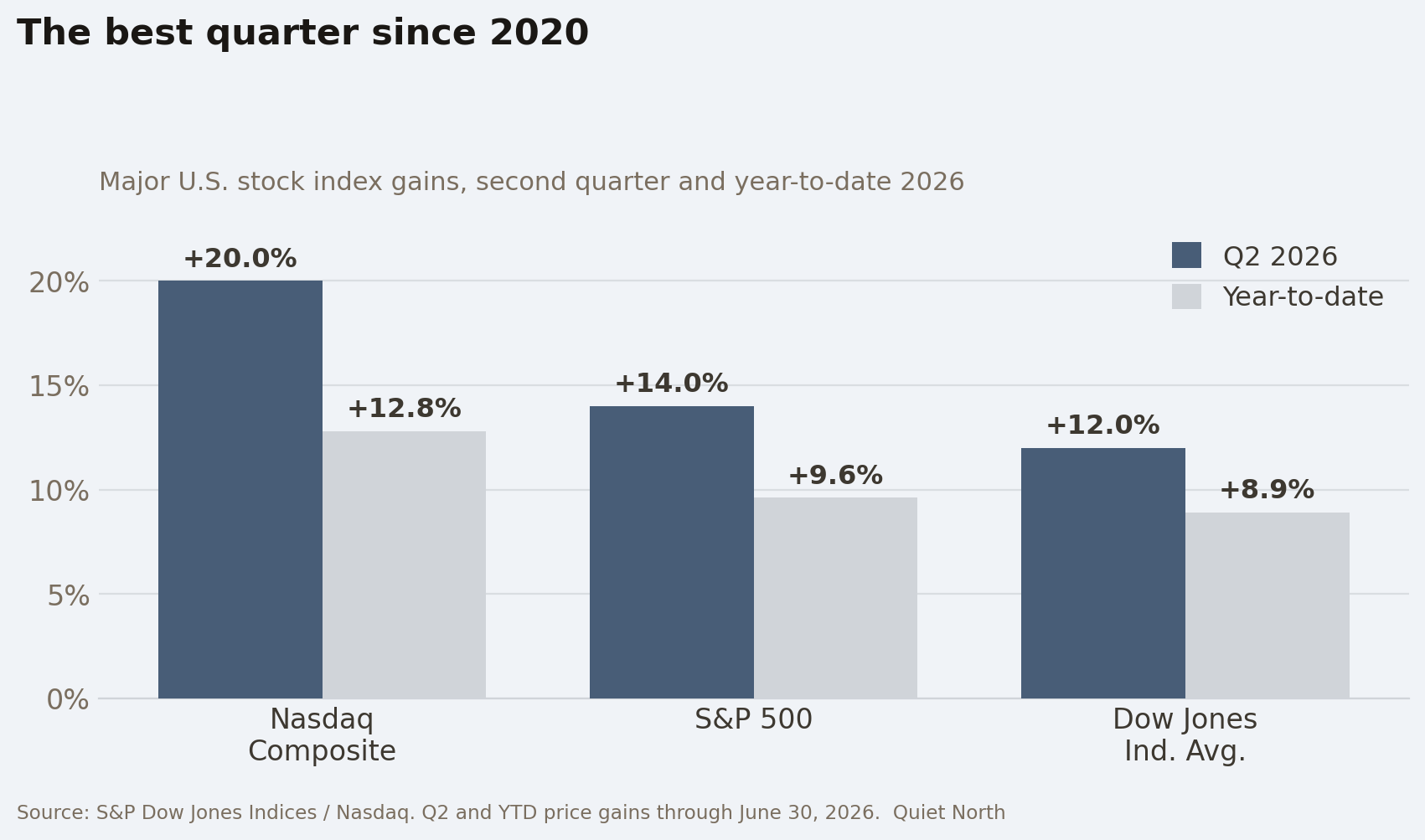

🔵 The first half of 2026 ended far more calmly than it began. On Tuesday, the major indexes closed the books on their best quarter since 2020 — the S&P 500 up about 14% for the three months, the Nasdaq roughly 20%, and the Dow around 12%, finishing at a record. That is a remarkable result for a stretch that also contained a Middle East war, a scare over AI spending, and an inflation reading that refused to cooperate. It is worth pausing on, not to celebrate, but because it carries a quiet lesson: the quarters that feel the most unsettling are rarely the ones that reward selling. Today, on the first morning of the second half, three things will shape what comes next. Here is what they are, and what each means for you.

Key points

- U.S. stocks closed the strongest quarter since 2020, with the Dow ending at a record 52,319.

- The Supreme Court affirmed the Federal Reserve's independence on Monday — an important, if narrow, ruling for long-term stability.

- The June jobs report arrives Thursday, July 2, a day early, before markets close for Independence Day.

Numbers like these can tempt two opposite mistakes: rushing in because things look good, or bracing for a fall because the gains feel too fast. The steadier path is to look at what actually drives the months ahead. This week, three forces stand out.

The Supreme Court kept the Fed independent — quietly, and narrowly

The most consequential news of the week was not a market move. On Monday, June 29, the Supreme Court ruled that the Federal Reserve holds "a measure of independence" from day-to-day politics — affirming that the president cannot simply remove its officials over policy disagreements. The case grew out of the administration's attempt to fire a sitting Fed governor.

Why does this matter to someone drawing on savings? Because the Fed's independence is one of the quiet foundations under your retirement portfolio. When a central bank is free to fight inflation without political pressure, long-term interest rates and the dollar tend to stay more stable — and stability is what protects the purchasing power of a fixed income. The ruling was narrow: the Court did not spell out how far that independence extends, and legal scholars noted the Fed is now the last independent agency of its kind. Still, for markets, the takeaway was reassuring. It removed, at least for now, one of the larger uncertainties hanging over the second half.

That reassurance arrives just as the Fed faces a genuinely difficult decision — and this week brings the data that will shape it.

Thursday's jobs report, and why the Fed is leaning the other way

For most of the past year, the expectation was that the Fed's next move would be a rate cut. That has flipped. After energy costs pushed inflation higher this spring, markets now price roughly a 65% chance of a rate hike by September, and about half of Fed policymakers favor one. New chair Kevin Warsh has said returning inflation to the 2% target is his priority.

This week's data will test that stance. A few markers to watch:

- Job openings held at 7.6 million in May — still firm, a sign the labor market has not weakened.

- The June jobs report lands Thursday, July 2, a day earlier than usual because markets close Friday for the holiday. Forecasters expect around 110,000 new jobs.

- A number much stronger than that would reinforce the case for a hike; a soft one would complicate it.

Here is what this means for you. Higher rates are a genuine mixed blessing for older Americans. They raise the cost of any new borrowing, and they can pressure rate-sensitive stocks like utilities and real estate. But they are quietly good news for savers, because they keep the yields on cash and bonds elevated. Which brings us to the most practical question of all.

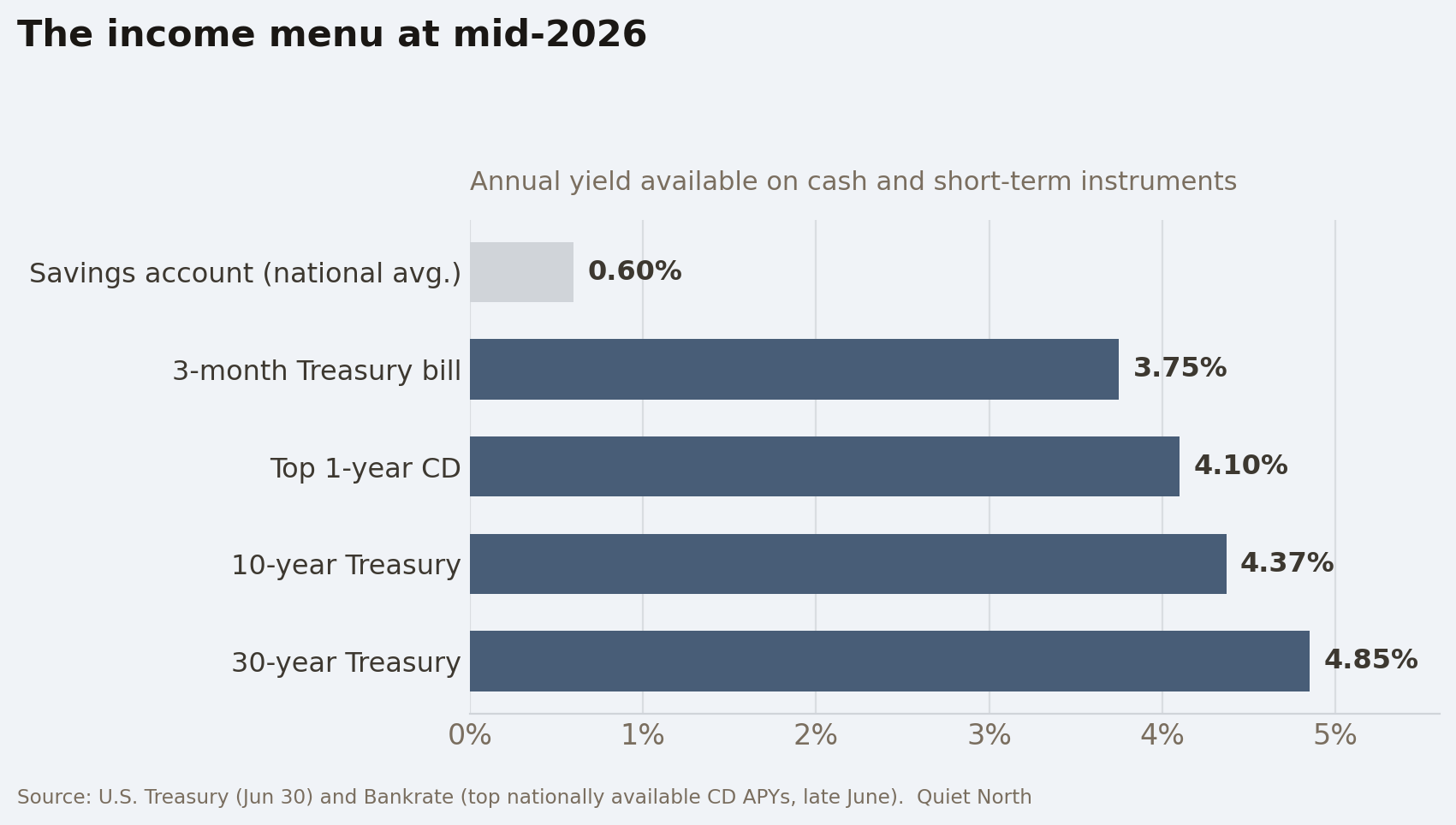

What steady income pays now — and what gold is doing

For readers who care about dividend income and safe yield, the picture at mid-2026 remains favorable, provided the money is actually working:

- A 3-month Treasury bill yields about 3.75%, and the top nationally available 1-year CDs pay roughly 4.00–4.15%.

- The 10-year Treasury sits near 4.37%, the 30-year near 4.85%.

- A typical savings account still pays under 1% — the real, avoidable cost of leaving cash idle.

Cash yields near 4% will not make anyone rich, but they do something valuable: they let conservative money keep close to pace with inflation while taking almost no risk. That is a meaningfully better position than savers faced for most of the decade before 2022.

Gold tells a different story this quarter. Spot prices traded near $4,000 an ounce this week, close to an eight-month low, down about 11% for the month and roughly 14% for the quarter — its steepest quarterly fall since 2013. The pressure is straightforward: a strong dollar and rising expectations of Fed rate hikes make a non-yielding asset less appealing when a Treasury pays over 4%. This does not erase gold's role as a long-term store of value and a currency hedge. It is a reminder that the role is patient and strategic — not a lever to pull in reaction to any single quarter. The same discipline that made this quarter's gains hold is the discipline that treats gold as ballast, not a bet..

🔍 What this means for you

The first half of 2026 rewarded patience. The second half will ask for the same. The practical reading of this week is calm:

- A strong quarter is a good time to review, not to chase. Records invite both greed and fear; a steady plan needs neither.

- The Fed ruling removed a real uncertainty. An independent central bank is a quiet ally of anyone living on a fixed income.

- Watch Thursday's jobs number, but don't trade on it. A hot report could revive rate-hike talk and some market volatility — normal for a thin holiday week, and not a reason for alarm.

- Income still pays. Near-4% yields on cash and short Treasuries remain one of the clearest opportunities for conservative savers in years.

I have watched a great many quarters begin with confident forecasts and end nothing like them. The value in a week like this is not prediction. It is orientation — knowing which few things actually matter, so the rest of the noise can pass by. The first half is closed. It ended better than it felt. The task now, as always, is to stay clear enough to let that steadiness continue. 🔔

Regards,

David Ellison