Why a weaker June jobs report lifted markets — and what it means for income, rates, and gold.

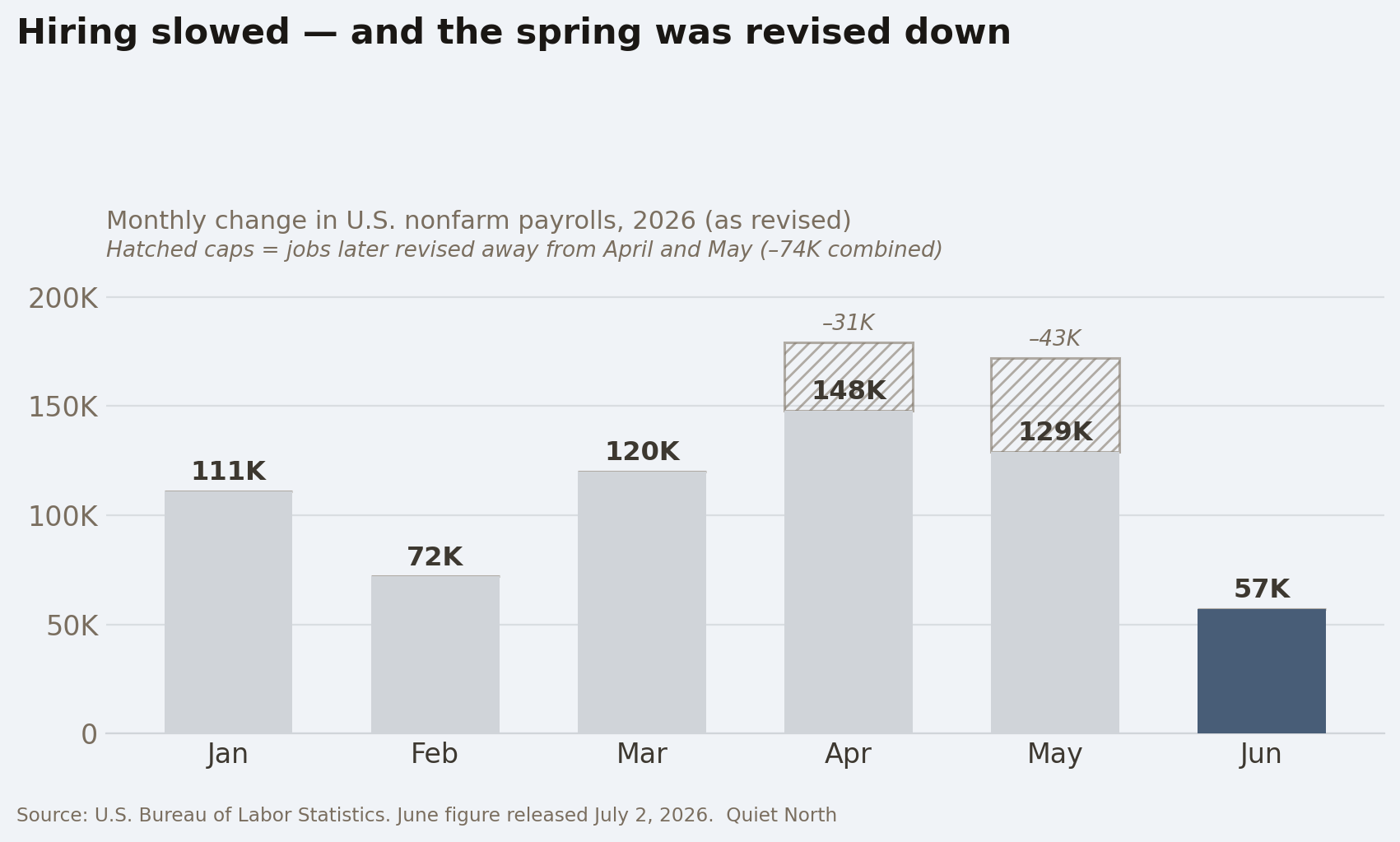

🔵 U.S. markets are closed today for the Independence Day holiday, which makes this a good morning to sit with a number that landed yesterday and quietly rearranged the second half of the year. The June jobs report showed the economy added just 57,000 jobs — roughly half what economists expected, and the weakest reading in four months. On its own, one soft month would be noise. But it arrived with downward revisions to April and May, and it did something unusual: markets rose on the disappointing news. Here is the calm explanation of why, and what it means for the things that matter to income and retirement.

Key points

- June payrolls grew by just 57,000, well below the roughly 115,000 expected, with 74,000 jobs revised away from April and May.

- The unemployment rate actually fell to 4.2% — but for a reason worth understanding.

- Markets and gold both rose as traders scaled back bets on a Federal Reserve rate hike; gold climbed back above $4,100.

Markets closed today — U.S. Independence Day holiday.

A weak jobs report that lifts the market can feel contradictory. The logic is straightforward once you see it: softer hiring makes the Federal Reserve less likely to raise interest rates, and lower rates are generally good for both stocks and bonds. For months, the worry had been that a hot economy would force the Fed to tighten. June eased that worry.

Why markets welcomed a weak report

Before yesterday, the odds of a Fed rate hike as soon as September sat near 67%. After the report, they fell below 50%, and traders pushed their expectations for any tightening further out into the year. The policy-sensitive 2-year Treasury yield dropped to about 4.13%.

This repricing rippled outward in ways that matter to older investors:

- Bonds rose as yields fell, lifting the value of existing fixed-income holdings.

- Gold jumped more than 2%, climbing back above $4,100 an ounce after a difficult month, as lower expected rates reduce the cost of holding a non-yielding asset.

- Rate-sensitive stocks — utilities, real estate, and dividend payers — tend to benefit when the threat of higher rates recedes.

None of this is a reason to celebrate a slowing economy. But it explains why a soft number can steady, rather than shake, a portfolio built for income. The market wasn't cheering fewer jobs; it was pricing in a gentler Fed.

There was, however, a detail beneath the headline that deserves a closer and more honest look.

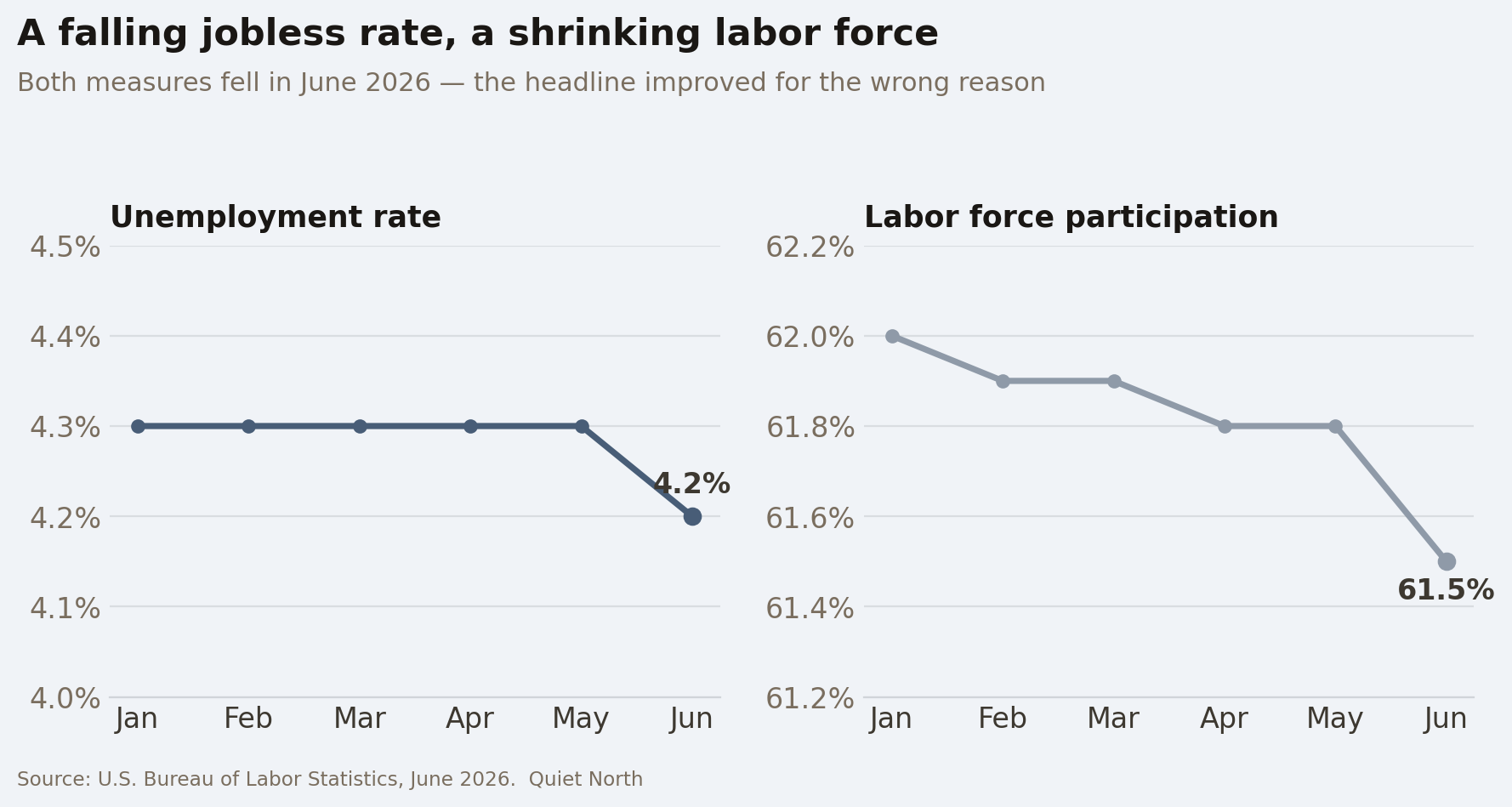

The unemployment rate fell — but not for a good reason

At first glance, the report contained a bright spot: the unemployment rate dropped to 4.2%, its lowest since June of last year. Ordinarily that would signal strength. This time, it didn't.

The rate fell because the labor force participation rate — the share of adults working or actively looking for work — declined to 61.5%, the lowest since March 2021. The household survey showed roughly 507,000 fewer people reporting that they were employed. When people stop looking for work, they are no longer counted as unemployed, so the rate can improve even as the underlying picture softens. In other words, the headline got better while the substance got a little weaker.

For older Americans, this is a useful reminder to read past the top-line number. A falling unemployment rate driven by people leaving the workforce is a very different thing from one driven by strong hiring. It is not cause for alarm — the labor market is cooling, not cracking — but it is a reason to treat the "good news" with a measure of care.

❓ Today's question

"If a weak jobs report is good for my investments, should I hope for more of them?"

It's an understandable thought, but no — and the reason is worth holding onto. Markets rose yesterday because one soft report eased fears of a rate hike, not because weakness itself is desirable. A single cooling month, against a backdrop of low unemployment and steady wages, is the "soft landing" many have hoped for. But a string of sharply weak reports would eventually signal a genuine slowdown, which tends to hurt corporate profits, employment, and the retirement accounts tied to both. The healthiest outcome for most savers isn't a weak economy or a red-hot one — it's a steady, moderate one that keeps inflation contained without tipping into recession.

🔍 What this means for you

Yesterday's report changed the near-term story more than most single numbers do. The practical reading stays calm:

- The rate picture has shifted toward patience. A softer job market gives the Fed room to hold steady at its July 29 meeting rather than hike.

- Income holdings just got a small tailwind. Falling yields lift existing bond values, and cash yields near 4% remain available for now.

- Gold reminded everyone what it's for. Its bounce came precisely when the rate outlook softened — a working example of safe-haven demand.

- Read past the headline. A lower unemployment rate built on a shrinking labor force is weaker than it looks. The trend in hiring matters more than any one month.

I have always found holidays useful for exactly this kind of reflection — a day when the market is closed and there is nothing to do but understand. Yesterday's number will shape headlines for weeks, but its real lesson is quieter: the economy is easing gently, the Fed has been handed room to wait, and the steady income that anchors a good retirement plan is, for now, still steady. Enjoy the holiday. The markets will be there Monday, and so will we. 🔔

Regards,

David Ellison