What a Tech-Led Pullback Reveals About Your Index Fun

🔵 Friday brought the market's sharpest drop in over a year, led by a small group of large technology stocks. For retirees, the more useful question isn't why it fell — it's how much of a "diversified" portfolio now rides on a handful of names.

- The Nasdaq fell about 4% on Friday — its worst session in more than a year — driven by a sharp pullback in semiconductor stocks, while the broader S&P 500 lost 2.6%.

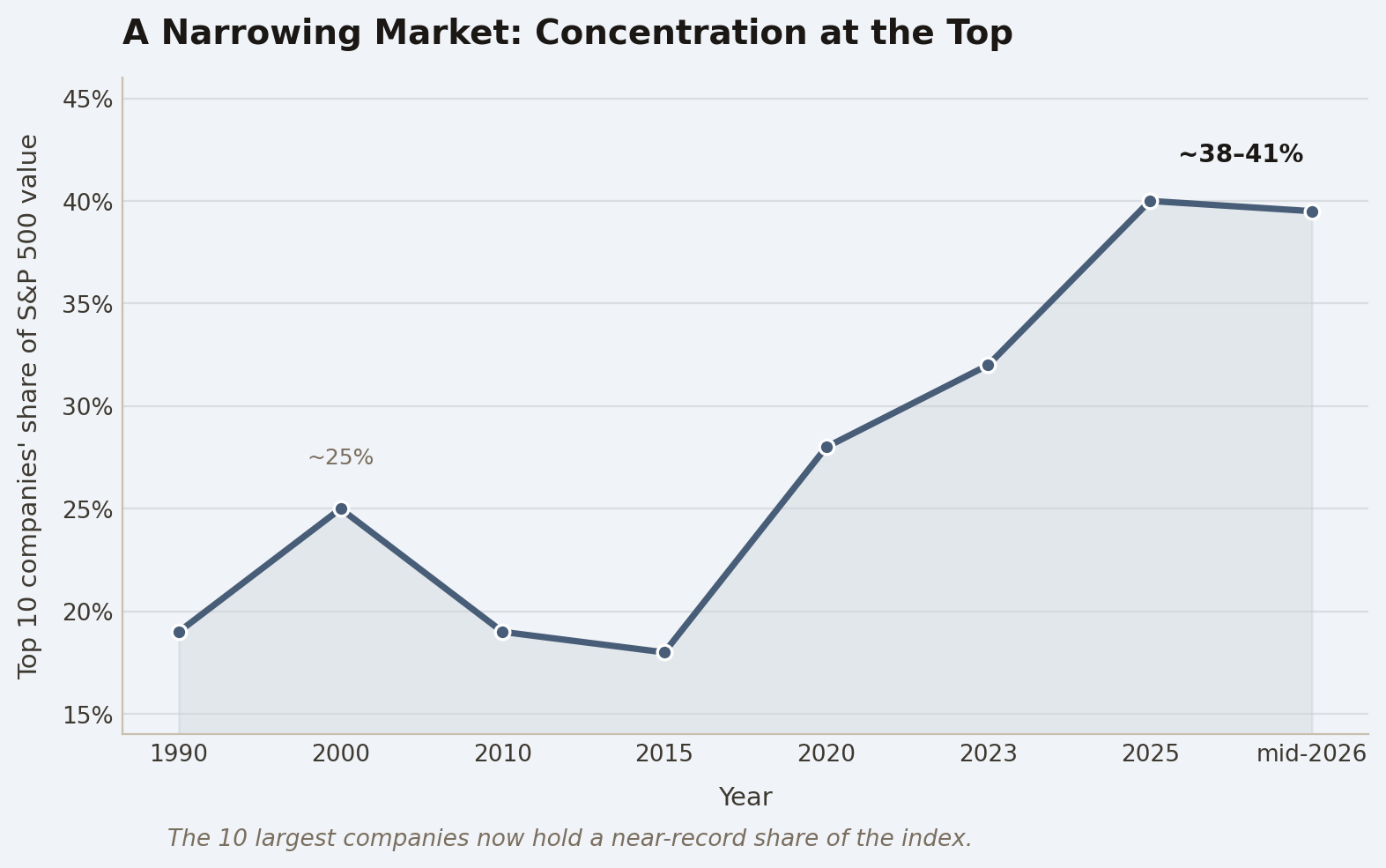

- The 10 largest companies now make up roughly 38–41% of the S&P 500, near a record, meaning a standard index fund is far less diversified than it appears.

- For income-focused retirees, the practical question is portfolio durability: how a few large stocks can move an entire account, and what genuine breadth looks like.

When a Few Names Move the Whole Market

The selloff, in plain terms. On Friday, the Nasdaq — the technology-heavy stock index — fell roughly 4%. That was its steepest single-day decline since April of last year. The broader S&P 500, which tracks 500 large U.S. companies, lost 2.6%.

On Monday, a major bank's trading desk shifted its stance to "tactically cautious," meaning it expects choppier trading in the weeks ahead. None of this is alarm. After a long winning streak, a pullback is historically normal — markets rarely climb in a straight line.The decline was concentrated in semiconductor stocks, the companies that design and make computer chips. A cautious outlook from one large chip supplier set the tone, and a stronger-than-expected May jobs report pushed interest rates higher the same day.

On Monday, a major bank's trading desk shifted its stance to "tactically cautious," meaning it expects choppier trading in the weeks ahead. None of this is alarm. After a long winning streak, a pullback is historically normal — markets rarely climb in a straight line.

Why does one rough session matter more to some people than others? Because timing changes everything. A retiree drawing income who sells into a decline locks in the loss permanently. The same drop barely touches a younger worker still adding money each month. In plain terms, that gap is called sequence-of-returns risk — the danger of poor returns arriving early, when you are spending the portfolio rather than building it.

Why so few stocks carried so much weight.

Here is the part that deserves your attention. The 10 largest companies in the S&P 500 now represent roughly 38% to 41% of the index's entire value. That is near the highest concentration on record, surpassing even the late-1990s peak.

When those few names fall together, a fund most people assume is broadly spread behaves like a narrow bet on a single theme. Many retirees hold a standard index fund, or a target-date fund built around one, and reasonably believe they own "the whole market."

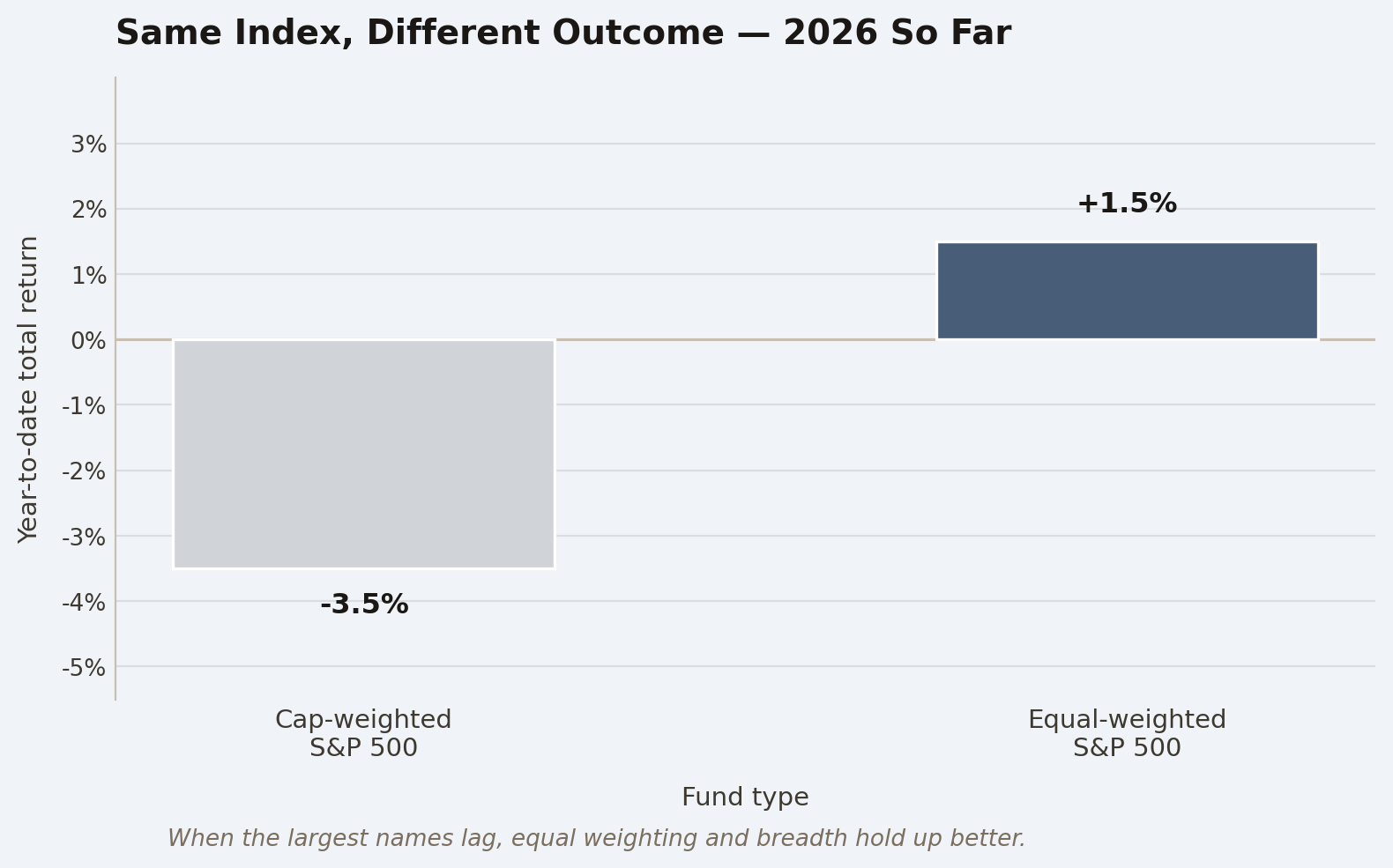

In practice, a large share of that money sits in a handful of companies. The equal-weight version of the same index — which gives each company the same slice rather than weighting by size — has held up better this year. That gap quietly shows how much the ordinary index now leans on its biggest members.

Separating the catalyst from the noise.

Two understandable forces converged on Friday: a cautious chip-sector outlook and a hot jobs report that lifted the 10-year Treasury yield — the government's benchmark borrowing rate — back above 4.5%. These were scheduled, explainable events, not a mystery.

The honest answer is that one strong session, or one weak sector, does not settle the larger question of whether these companies are priced for perfection. Worth noting: yields and oil had been moving in step for weeks. Friday they parted ways, as the chip story took over. The drivers shift from week to week, which is exactly why reacting to any single headline tends to cost more than it helps.

What "Diversified" Actually Means for Retirement Income

In everyday terms, diversification means spreading risk so no single company or theme can sink the whole portfolio. The quiet irony of a cap-weighted index fund — one that weights companies by size — is that it works against that instinct. As the largest names rise, they take up more room, and your exposure to them grows whether you intended it or not.

Durability usually matters more than maximum return. A portfolio that can absorb a tech-led drop without forcing you to sell at a bad moment is doing its job. The point is not to predict the next move. It is to understand the tradeoff you are carrying — and to notice that steadier income today can come from dividends, short-term Treasuries, and cash, which now pay competitively. Concentration in a few growth names is not the only lever for income.

This reminds me of the year 2000, when the index's largest members — Cisco, Microsoft, Intel — reached a share of the market that felt, at the time, simply like the natural order of things. I remember how reasonable it seemed to assume the leaders would keep leading. What followed was a long, uneven reset that rewarded breadth over the next several years. I am not predicting a repeat; nobody knows the timing of these things. But today's concentration has surpassed even that level, and that history is a useful reminder that leadership is not permanent. This is where patience matters.

❓ Today’s Question

"If the biggest stocks are driving most of my index fund's returns, does that mean I should move money into an equal-weight fund — and what would I be giving up if I did?"

Short answer: Not necessarily — it depends on what you want the money to do. An equal-weight fund gives each company the same slice, so it leans less on the largest names and tends to hold up better when they stumble. The tradeoff is real: during the years when a few giants lead, equal weight usually lags, and it can carry slightly higher fees and more turnover.

So the honest answer is that one structure is not simply "better" than the other; they suit different needs, and breadth tends to reward patience rather than quick results. The concrete step this week: pull up your main fund's fact sheet, find the top-10 weight, and compare it against an equal-weight version of the same index — that single comparison shows you the tradeoff in plain numbers.

I have learned over many cycles that the loudest market days rarely require the biggest decisions. Friday felt dramatic, but the useful work it prompts is quiet — opening a fund statement and reading what you actually own. Most of the time, that look is reassuring; occasionally it surprises you, and either way you are better off knowing. Understanding what you hold is not the same as needing to change it.

Clarity, more than action, is what lets a portfolio — and the person who owns it — stay steady. 🔔

Regards,

David Ellison