What the New Fed Chair Means for Your Interest-Rate Outlook

🔵 Kevin Warsh chairs his first FOMC meeting in two weeks — with inflation running at 3.8%, the most divided committee in decades, and markets now pricing in a possible rate hike instead of cuts.

Here is what changed, and what it means for bonds, cash, and retirement income.

Key Points

- The Fed's June 16–17 meeting will be Kevin Warsh's first as chair, and it arrives with updated economic projections (the dot plot) that will signal whether policymakers see rates rising, holding, or falling from here.

- Markets have shifted from expecting rate cuts to pricing in a roughly 50% probability of a rate hike by December 2026 — a reversal that directly affects bond prices, CD yields, and the income side of a retirement portfolio.

- Former chair Jerome Powell warned on June 1 that the Fed faces a political "stress test" — and the independence of the central bank has real implications for how confidently markets can trust the rate path ahead.

The New Fed: What Changed and Why It Matters Now

Last week, this newsletter looked at what enters your portfolio when a massive new company joins an index fund. This week is about the interest-rate environment that shapes what your portfolio earns. Both matter — but right now, the rate question is the one with the most moving pieces.

Three things converged in the past few days. Kevin Warsh officially took over as Fed chair. Jerome Powell delivered a pointed public warning about the central bank's independence. And the market's expectation for the direction of interest rates completed a reversal that has been building for months. Here is what each of those developments means, and why they add up to a picture every income-focused retiree should understand clearly.

Warsh Takes the Chair: What to Expect on June 16–17

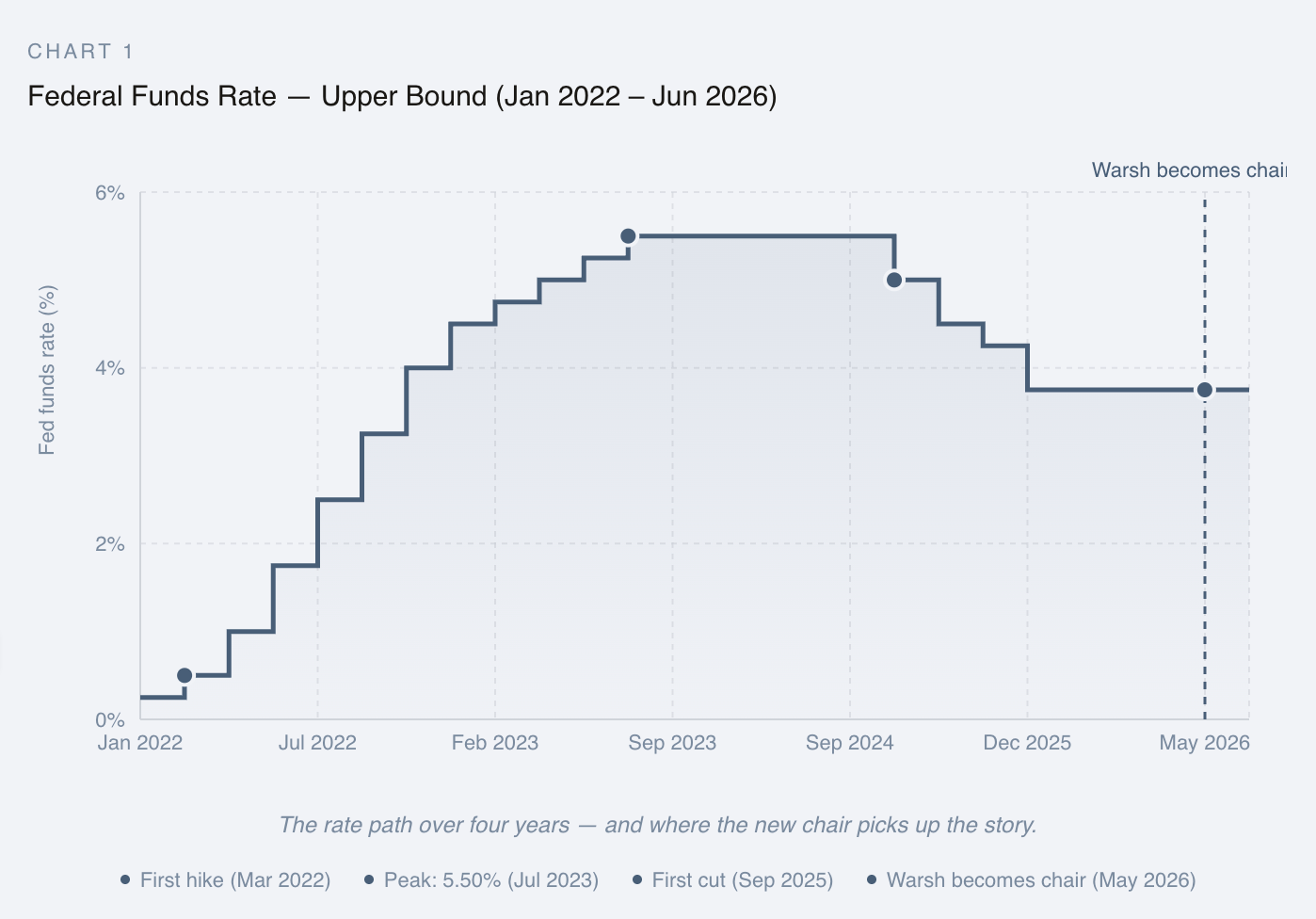

Kevin Warsh was sworn in as the 17th chair of the Federal Reserve on May 22, following a narrow 54–45 Senate confirmation — the most divisive vote for a Fed chair in the institution's history. His first FOMC meeting is now two weeks away, scheduled for June 16–17.

That meeting matters more than most. It is what the Fed calls a "projections meeting," meaning it includes not just a rate decision but also updated economic forecasts and the dot plot — a chart that shows where each individual committee member expects interest rates to go over the next one to three years. In plain terms, the dot plot is a vote-by-vote map of the committee's collective thinking about the future. It is not a promise. It is not a commitment. But it is the single most closely watched signal for the direction of rates, and it moves markets.

The reason this particular dot plot carries extra weight is context. The April FOMC meeting saw four of twelve voting members dissent from the rate decision or the policy statement. That is the most divided the committee has been since 1992. Warsh has indicated publicly that he favors lower rates, but the inflation numbers he has inherited make cuts difficult to justify. The central tension of his chairmanship begins on June 16: can the new chair steer a fractured committee toward a coherent policy path, or will the internal disagreement deepen?

Markets currently price roughly a 65% probability that the Fed will hold rates steady in June. That is the expected outcome. The real question is what the dot plot signals for the rest of 2026 and into 2027 — and that is where the uncertainty sits.

Inflation at 3.8% and the Rate-Hike Reversal

The inflation picture has changed more than most people realize. April CPI came in at 3.8% year-over-year — the highest reading since May 2023. Core CPI, which strips out food and energy, was 2.8%, still well above the Fed's 2% target. Energy costs rose 17.9% from a year earlier. Gasoline alone was up 28.4%.

But the number that caught the most attention was this: real average hourly wages — what workers actually earn after adjusting for price increases — fell 0.5% in April. For the first time in three years, inflation is outrunning wages. That matters for everyone, but it matters most for retirees on fixed income, because there is no next raise coming. Social Security cost-of-living adjustments try to compensate, but they lag the actual price increases by months.

Here is the shift that changes the landscape. As recently as late 2025, markets were pricing in two to three rate cuts for 2026. That expectation has completely reversed. Fed futures now show virtually zero chance of a cut through the end of 2027. Instead, the probability of a rate hike by December has risen to roughly 51%, with a 60% chance of a hike by January 2027.

That is a sea change. Most retirees who set up bond portfolios or CD ladders in 2025 were operating under the assumption that rates were heading lower. If the next move turns out to be a hike instead of a cut, the math on duration, yield, and portfolio positioning looks meaningfully different.

Three dates are worth marking on a calendar. June 5 brings the May jobs report — a fresh reading on whether the labor market is cooling or holding firm. June 10 brings the next CPI release — the final inflation data point before the FOMC meeting. And June 16–17 is the meeting itself: Warsh's first press conference, the new dot plot, and the first real signal of where this new Fed is heading. Those three reports, in sequence, will shape the rate outlook for the rest of the year.

What Rate Uncertainty Means for Bonds, Cash, and Income

The practical question is not whether to panic — there is no reason to. The practical question is whether you know how your income sources respond to the two possible outcomes: rates stay here, or rates go up.

I remember watching the last time a Fed chair inherited this kind of uncertainty. In February 2006, Ben Bernanke succeeded Alan Greenspan after Greenspan had raised rates seventeen consecutive times. Bernanke walked into a committee that was divided over whether to keep hiking, pause, or signal that cuts were coming. Inflation was creeping higher. Housing was overheating. Nobody knew which way the new chair would lean. Bernanke raised rates twice more, then paused. Markets wobbled through the uncertainty but eventually adjusted once his intentions became clear. The fog lifted — not because the data improved, but because the new chair's pattern of decision-making became readable. That is what markets are waiting for now. Warsh will become readable — but not on day one.

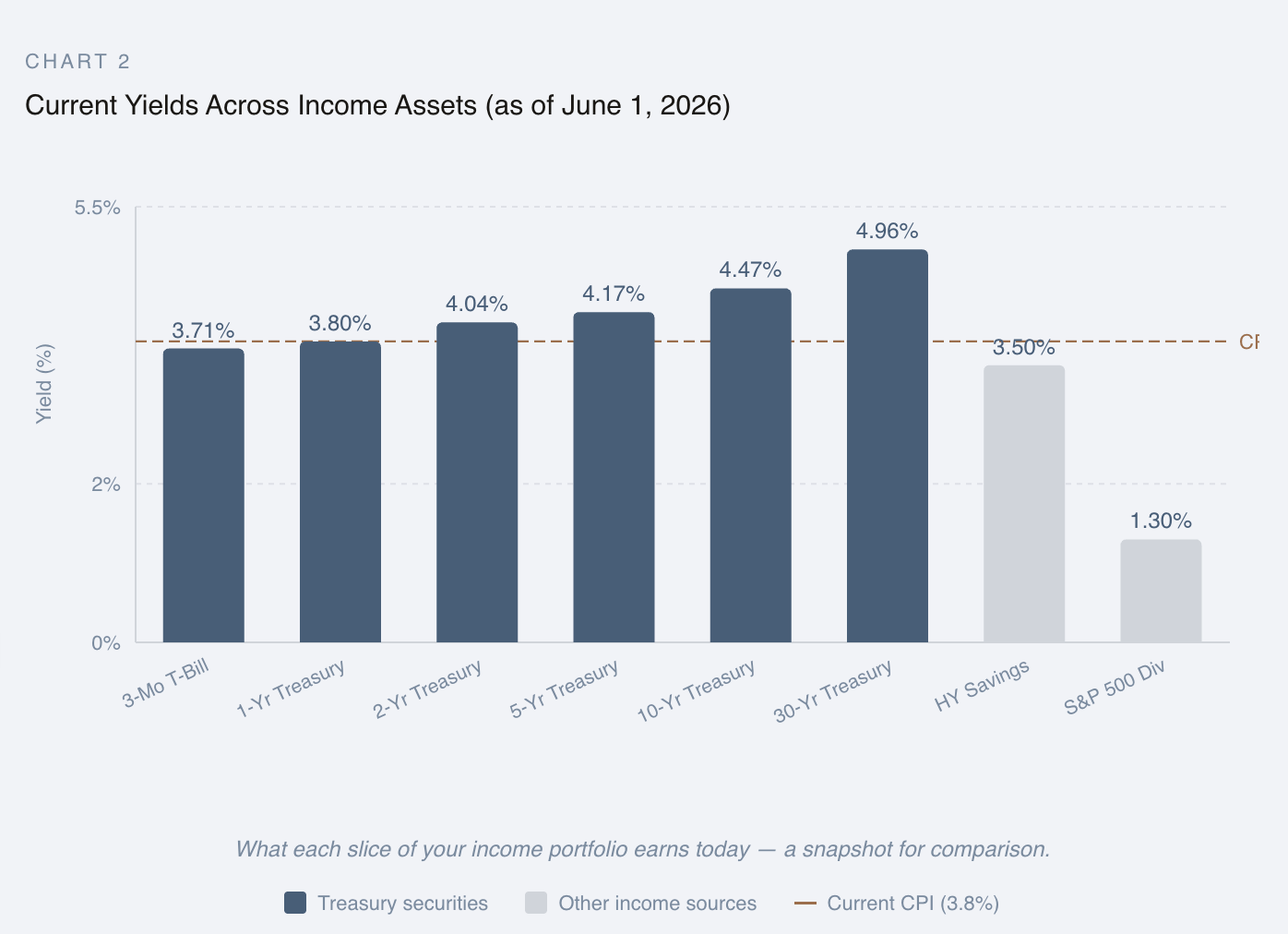

For cash and CDs, the picture is different. The 3-month Treasury bill pays 3.71%. The 1-year Treasury pays 3.80%. If a rate hike comes, those yields may rise further, which rewards patience in CD-ladder timing. If no hike comes, current short-term rates are likely close to their ceiling. Either way, cash held in a bank savings account paying less than 3% is earning less than what Treasuries offer today — and that gap adds up month by month.

I remember watching the last time a Fed chair inherited this kind of uncertainty. In February 2006, Ben Bernanke succeeded Alan Greenspan after Greenspan had raised rates seventeen consecutive times. Bernanke walked into a committee that was divided over whether to keep hiking, pause, or signal that cuts were coming. Inflation was creeping higher. Housing was overheating. Nobody knew which way the new chair would lean. Bernanke raised rates twice more, then paused. Markets wobbled through the uncertainty but eventually adjusted once his intentions became clear. The fog lifted — not because the data improved, but because the new chair's pattern of decision-making became readable. That is what markets are waiting for now. Warsh will become readable — but not on day one.

What This Means For You

None of this requires an immediate reaction. Warsh has not chaired a meeting yet. The June data has not been released. The point this week is not to act — it is to measure. Know what you hold, know how it responds to rate changes, and know what dates matter. That puts you ahead of the noise when it arrives.

- Pull up the duration number on every bond fund or bond ETF you hold — it is listed on the fund's fact sheet or summary page. A duration of 6 means the fund loses roughly 6% of its value for every one percentage point rise in interest rates. If a rate hike is possible by year-end, knowing your duration exposure tells you how much is at stake.

- Check the yield on any cash you hold in a bank savings account versus the current 3-month T-bill rate (3.71%) and 1-year Treasury rate (3.80%). If your savings account pays less than 3%, that gap represents income you are leaving on the table every month. Treasury money market funds and short-term T-bill ladders are worth comparing.

- Mark three dates on your calendar: June 5 (jobs report), June 10 (CPI release), and June 16–17 (Warsh's first FOMC meeting with new projections). These three data points, in sequence, will shape the interest-rate outlook for the rest of 2026. You do not need to act before them — but knowing they are coming helps you avoid reacting to noise in between.

❓ Today’s Question

"If the Fed does raise rates later this year, what happens to the bond funds I already own — and is there a way to reduce that sensitivity without selling everything?"

Short answer: When interest rates rise, bond fund prices decline — that is mechanical, not a sign of a broken fund. The amount of the decline depends on the fund's duration. A fund with a duration of 6 would lose roughly 6% of its market value for each percentage point of rate increase. One approach some investors use to reduce that sensitivity is shifting a portion of their bond allocation toward shorter-duration funds — funds that hold bonds maturing in one to three years instead of ten to twenty.

Shorter-duration funds are less sensitive to rate moves, though they also tend to pay lower yields. This is not a recommendation — it is a tradeoff worth understanding. A concrete step you can take this week: look up the duration of every bond fund you hold, then compare it against a short-term Treasury fund like a 1–3 year Treasury ETF to see the difference in both yield and rate sensitivity.

The Fed is changing hands, and the honest answer is that nobody — not the market, not the new chair, not the old one — knows exactly where rates are heading. That uncertainty is uncomfortable. But it is also familiar. I have watched several of these transitions, and the pattern is always the same: a period of fog, followed by a period of clarity, once the new chair's decision-making becomes readable. The useful work right now is not prediction. It is preparation — knowing what you own, knowing how it responds, and having the patience to wait for the fog to clear. That is what steady looks like. 🔔

Regards,

David Ellison