When Bonds Catch a Break: A Quiet Week in Treasury Yields

🔵 Treasury yields eased to their lowest level in more than two weeks as oil tumbled on tentative ceasefire progress.

Treasury yields eased to their lowest level in more than two weeks as oil tumbled on tentative ceasefire progress. Here is what a quieter bond market does to retirement income — and what it does not.

Key Points

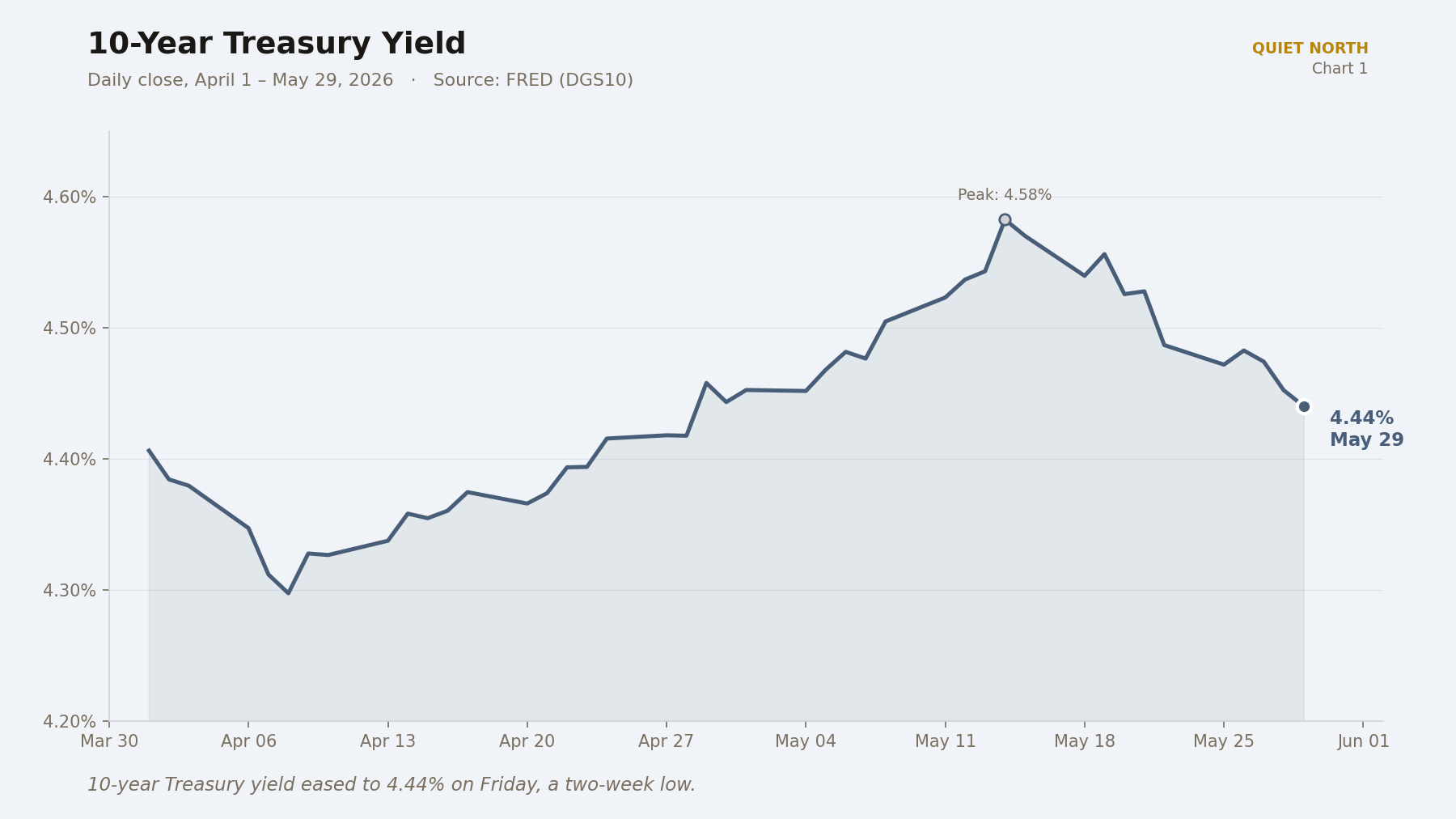

- The 10-year Treasury yield closed at 4.44% on Friday, its lowest in more than two weeks, after reports that US and Iranian negotiators had "mostly agreed" on a 60-day ceasefire extension.

- Brent crude is down nearly 19% for May, the steepest monthly drop since April — energy is moving from a source of inflation pressure toward, at least temporarily, a source of inflation relief.

- Even so, markets still embed roughly a 46% probability of a December rate hike, meaning the Fed's next move is genuinely uncertain and worth pricing into income decisions.

A Quieter Bond Market

Yields ease as a ceasefire takes shape

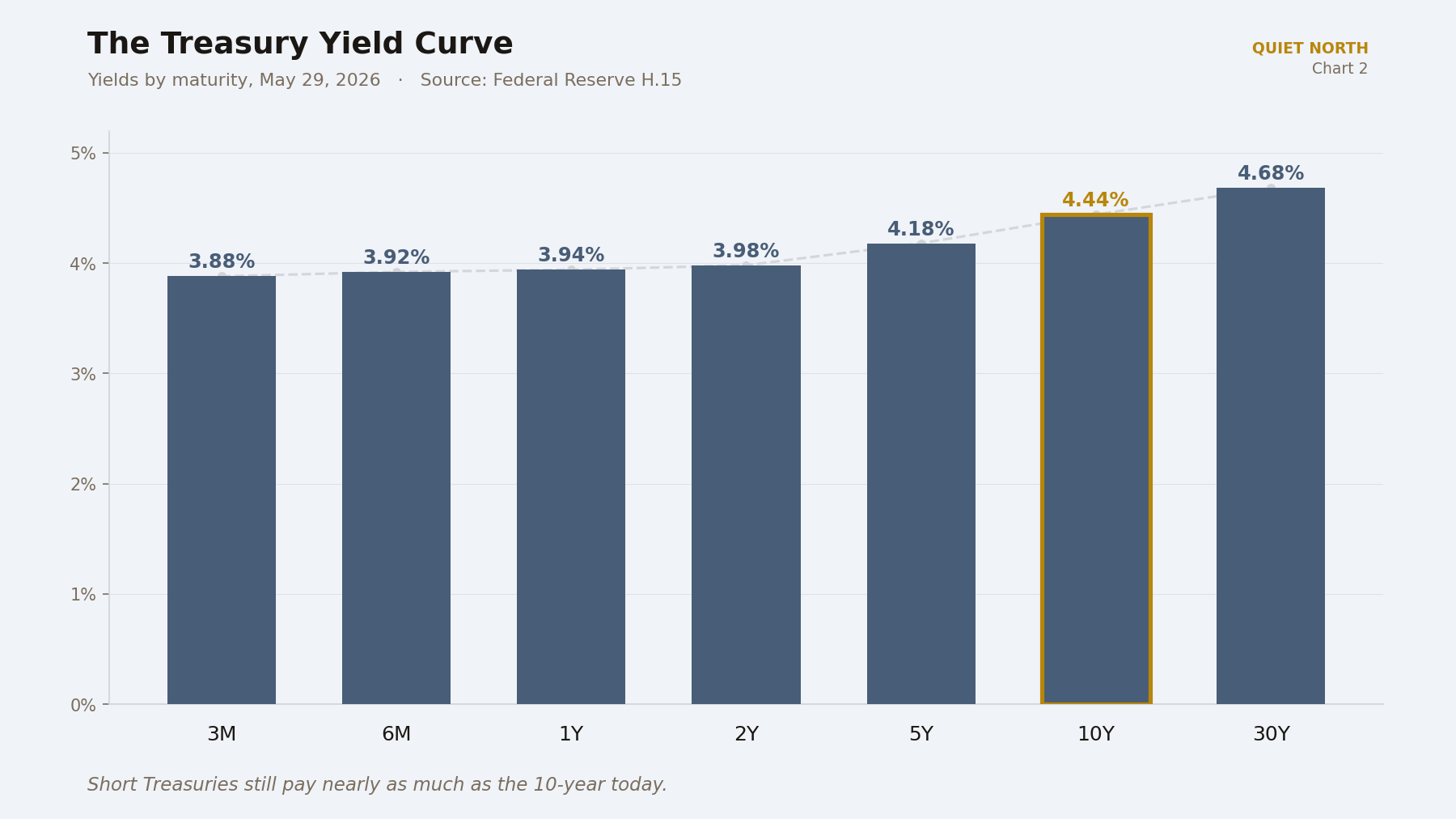

The 10-year Treasury yield finished Friday at 4.44%, its lowest level since mid-May. The 2-year — generally a better read on near-term Fed expectations — ended at 3.98%. The move followed reports that US and Iranian negotiators had reached an in-principle 60-day memorandum of understanding, or MOU — in plain terms, a draft agreement that still needs sign-off. The MOU would extend the ceasefire and begin nuclear-program talks; President Trump has not yet formally approved the terms.

A move from above 4.50% to 4.44% does not sound like much. In bond terms, it is meaningful. Six basis points — one basis point equals 0.01 percentage point — on a benchmark borrowing rate touches mortgages, corporate loans, and the price of every bond fund a retiree might own.

The chain runs in a familiar order. Less war risk leads to lower oil; lower oil softens the inflation outlook; a softer inflation outlook reduces the case for holding policy rates higher for longer. None of those links is automatic, but the bond market traded the sequence this week.

Worth noting: this is a calmer week, not a trend reversal. The 10-year has moved 30 basis points or more in either direction within a single week several times this year. One quieter Friday is a data point, not a forecast.

Oil's reversal, and what it changes

Brent crude is down nearly 19% for May, on track for its steepest monthly drop since April. West Texas Intermediate, the US benchmark, ended Friday near $87.69 a barrel. The decline tracks the same ceasefire optimism — markets are pricing the possibility of normalized shipping through the Strait of Hormuz, the narrow waterway through which roughly a fifth of global oil moves each day.

Last week's letter looked at how a hotter inflation print was pressing on budgets, with energy doing most of the lifting. This week, some of that pressure eased.

A sustained 19% drop in crude tends to show up at the pump within weeks, and in heating and electricity bills shortly after. Energy is the line item retirees can least skip — the lower oil moves, the less of a real hit a fixed income takes from prices that cannot be adjusted around. That is relief, not victory, and very capable of reversing.

The Fed sits, but markets haven't ruled out a hike

Thursday's PCE release — PCE meaning Personal Consumption Expenditures, the Federal Reserve's preferred inflation gauge — showed both headline and core monthly readings coming in below expectations. Softer than feared. Annual readings, however, remained well above the Fed's 2% target, at 3.8% headline and 3.3% core.

Even with that softer print, market pricing on Friday still showed roughly a 46% probability of a December rate hike. That figure comes from federal funds futures — contracts that let traders bet on future Fed decisions — and is the market's own probability, not a forecast from any single forecaster. The Fed has held its benchmark rate at 3.50% to 3.75% since the April 29 meeting.

In plain terms, a 46% probability of a December hike is the market saying the next move is roughly a coin flip, leaning slightly toward "no change." It is not a forecast — it is a price. That price is more honest than the simpler "rates are coming down" story heard in many headlines.

Why a Quieter Bond Week Matters for Income

A week of easing yields shifts two things at once for a retirement portfolio. New money put to work pays a little less when yields drift down. Existing bond fund holdings, on the other hand, rise in price, because their fixed payments look more attractive than what is now being offered. The word for that price sensitivity is duration, listed on each fund's fact sheet under "average effective duration" — a duration of 6 means roughly a 6% price gain if yields drop 1 percentage point, and a 6% loss if they rise 1 point.

This reminds me of 1990 and 1991. Iraq's invasion of Kuwait that August pushed oil from around $20 a barrel to above $40 within weeks; after the coalition's campaign and ceasefire in February 1991, oil collapsed back below $20 by April, and Treasury yields drifted lower across the following months. I watched retirees who had stretched for the spike's higher yields find them no longer available a few months later. The lesson then, and now, is that geopolitically driven yield moves can reverse as quickly as they arrive — in both directions.

Social Security is the other half of the picture. The cost-of-living adjustment for this year is already set, and does not change on Friday's news. Treasury and bond income is what can actually shift week to week — and that is where this week's news lands, on the income that adjusts, not the income that holds.

What This Means For You

None of this calls for a sudden move. A 60-day MOU has not yet been approved, oil prices can move back, and the Fed's next step is roughly a coin flip in the market's own pricing. The useful work this week is measurement — knowing what every piece of your income is actually doing while the bigger questions sit unresolved.

- Write down the duration of any bond fund you own — it is usually printed on the fund's fact sheet under "average effective duration." Then translate it: a duration of 6 means roughly a 6% price gain if yields drop 1 percentage point, and a 6% loss if they rise 1 point. That single number tells you how exposed the fund is to weeks like this one, in both directions.

- Check the current yield on any cash sitting in a checking account, a standard savings account, and a government money-market fund or short Treasury fund — side by side, on one page. The point is not to chase the highest yield. It is to know how far apart the three numbers actually are. Today, the gap is still meaningful.

- If you hold a CD ladder, list each rung: what rate it pays and when it matures. Note which one rolls next. Lower yields between now and then would mean a lower replacement rate at that rung — which is useful to see in advance rather than discover at the renewal letter.

❓ Today’s Question

"If bond yields are starting to drift down, should I be locking in longer-dated Treasuries or longer CDs now to capture today's rates before they fall further?"

Short answer: The honest answer is that one calmer week is not the same as a trend, and 4.44% on the 10-year — down from above 4.50% — is meaningful in bond terms but small in the context of a year that has seen 30-basis-point swings both ways. The deeper question is not "what will yields do next?" but "what is this money for?" Money you will not touch for many years tolerates the duration risk of longer bonds, because the price swings smooth out over time. Money you may need within a year or two for living expenses does not.

A practical step you can take this week without calling anyone: look up the maturity dates on any longer-dated Treasuries or CDs you already own, and write the date each one matures next to the rate it pays. That single page tells you what locked-in income you already have — before deciding whether you need more of it.

A quieter week in bonds is, oddly, harder to write about than a noisy one. There's no headline to react to, no sharp move to explain — just a small step down in yields, a softer print, and an oil chart that turned the other way. I've learned over the years to treat weeks like this one as the time to look at my own statements rather than the news, because the noise is what changes and the statements are what matter. The picture this Friday is calmer than the picture two Fridays ago; whether it stays that way is not for me to say. I'm grateful for the quieter window while it lasts. 🔔

Regards,

David Ellison